CORRESP: A correspondence can be sent as a document with another submission type or can be sent as a separate submission.

Published on January 2, 2018

January 2, 2018

Via EDGAR Submission

U.S. Securities and Exchange Commission

Division of Corporation Finance

100 F St. Street, NE

Washington, D.C. 20549

Attn: Jennifer Thompson, Accounting Branch Chief

Sondra Snyder, Staff Accountant

Elizabeth Sellars, Staff Accountant

RE:

Clean Energy Fuels Corp.

Form 10-K for Fiscal Year Ended December 31, 2016 Filed March 7, 2017

Form 10-Q for Fiscal Quarter Ended September 30, 2017 Filed November 2, 2017

File No. 001-33480

Dear Ms. Thompson:

Clean Energy Fuels Corp. (the “Company”) is submitting this letter in response to comments received from the staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”) in a letter dated December 15, 2017 (the “Comment Letter”) with respect to the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2016 (File No. 001-33480) filed with the Commission on March 7, 2017 (the “Annual Report”), and the Company’s Quarterly Report on Form 10-Q for the fiscal quarter ended September 30, 2017 (File No. 001-33480) filed with the Commission on November 2, 2017 (the “Quarterly Report”).

For your convenience, the Staff’s headings and comments set forth in the Comment Letter have been reproduced in bold and italicized font herein with responses immediately following each comment. Defined terms used herein but not otherwise defined herein have the meanings given to them in the Annual Report and the Quarterly Report.

****

Form 10-Q for Fiscal Quarter Ended September 30, 2017

Financial Statements

Note 2 – Asset Impairments, Other Charges and Inventory Valuation Provision, page 7

1. |

We note from your disclosures that as a result of the asset impairments recorded during the third quarter you determined that sufficient indicators of impairment existed to trigger interim goodwill impairment testing and that as a result of that testing you concluded that it was more likely than not that the fair value of your reporting unit exceeded its carrying value at September 30, 2017 and no impairment was required. It appears that at September 30, 2017, based on the price of your common stock as of September 29, 2017, the net book value of your stockholders’ equity exceeded your market capitalization by approximately $91.1 million. In |

1

order to help us understand how you determined the fair value of your reporting unit, please address the following comments:

• |

Tell us how you determined that you have a single reporting unit. |

• |

Tell us in reasonable detail how you determined the fair value of your reporting unit. Please include the specific method(s) utilized. |

• |

Tell us the material assumptions used under each method utilized. Examples might include: how cash flows were estimated, the discount rate used, the principal market and market participants selected. Please ensure your response addresses how you determined each of the assumptions used was appropriate. |

• |

If you utilized multiple approaches in determining fair value, please tell us the relative weighting assigned to each method and how you determined the weighting was appropriate. |

• |

Please provide us with a reconciliation of the fair value of your reporting unit to your market capitalization. If applicable, provide support for any control premiums. Refer to ASC 350-20-35-22 and -23. |

Response:

The Company acknowledges the Staff’s comments and respectfully advises the Staff that although the Company’s net book value of stockholders’ equity exceeded its market capitalization by approximately $91.1 million at September 30, 2017, the fair value of the Company’s reporting unit exceeded the net book value of stockholders’ equity at such date and thus no goodwill impairment was required. A discussion of the Company’s assessment to arrive at this determination is provided below by separately responding to each of the Staff’s individual comments.

• |

Tell us how you determined that you have a single reporting unit.

|

Response

The Company determined that it has a single reporting unit in accordance with Accounting Standards Codification (“ASC”) 350, which defines a reporting unit as an operating segment (i.e., before aggregation or combination), or one level below an operating segment (i.e., a component).

The Company has one operating segment comprised of the following activities or components (“the Components”) at September 30, 2017:

• |

Selling CNG, LNG, and RNG fuel (“natural gas”) and providing operation and maintenance (O&M) services to the associated customer-owned fueling stations. |

• |

Designing and constructing natural gas fueling stations and facility modifications and selling those to customers. |

• |

Selling natural gas fueling compressors and related equipment and maintenance services. |

The Company determined it had one operating segment using the criteria set forth in ASC paragraph 280-10-50-1 which states that an operating segment is a component of a public entity that has all of the following characteristics:

a. |

It engages in business activities from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same public entity). |

2

b. |

Its operating results are regularly reviewed by the public entity’s chief operating decision maker (“CODM”) to make decisions about resources to be allocated to the segment and assess its performance. |

c. |

Its discrete financial information is available. |

The Company determined that each of the Components satisfied criteria (a) and (c) but none of the Components satisfied criterion (b). As a result, because all of criteria (a), (b) and (c) must be satisfied for a component to be considered an operating segment, the Company determined that none of the Components was a separate operating segment and rather all of the Components collectively comprised the Company’s one, single operating segment.

The Company determined that none of the Components satisfied criterion (b) by assessing the manner in which the CODM reviews the Company’s operating results.

In addition, the Company considered the guidance in ASC 350-20-35-34 that states a component of an operating segment is a reporting unit if the component constitutes a business for which discrete financial information is available and segment management, as that term is defined in paragraph 280-10-50-7 and 8, regularly reviews the operating results of that component.

The Company’s Chief Executive Officer is the Company’s CODM and the segment manager because he is the individual primarily responsible for making the operating decisions of the Company. In reviewing and evaluating the Company’s operating performance, the CODM assesses the Company in light of its business strategy, which is to build a foundation through the Company’s and its customers’ distribution networks to support the anticipated growth in the use of natural gas as a vehicle fuel. This strategy is heavily dependent upon the broad adoption of natural gas as a main fuel source for commercial and industrial vehicles, and the CODM views all of the Components as parts of one integrated plan to stimulate this adoption and execute on the Company’s business strategy. In his review and assessment of the Company’s operations, the CODM primarily focuses on aspects of the Company’s operations that, in his view, are indicators of the Company’s implementation of this business strategy.

The CODM obtains information primarily through reviewing consolidated volume and financial information and reports provided by the Company’s Chief Financial Officer (“CFO”) at Executive meetings and presentations to Company’s Board of Directors. The frequency and content of information received is detailed below.

On a monthly basis, the CODM receives the following:

• |

A volume report which contains the volume of CNG, LNG and RNG gasoline gallon equivalents delivered. |

The CODM regularly reviews volume of CNG, LNG and RNG delivered, as volume delivered is the overarching key metric that allows the CODM to assess the overall financial performance of the Company. The CODM uses this information to make company-wide and timely decisions related to investment in infrastructure and other capital commitments, changes in personnel, dispatching corporate employees to assist in operational improvement, and the allocation of any other Company resources.

The CODM receives the information below at bi-monthly executive meetings and quarterly Board of Directors meetings:

3

• |

Volume, volume-related revenue and gross margin by market sector (trucking, refuse, transit, fleet services and bulk delivery) and by volume type (O&M, fuel, and fuel and O&M), and any fueling station revenues and gross margin by market sector. |

• |

Consolidated profit and loss statements with volume, and per gallon delivered gross margin, including revenues as disclosed in the key operating data section of the Annual Report and Quarterly Report and their related gross margin, consolidated SG&A, net income and Adjusted EBITDA. |

During executive and Board of Directors meetings, the CODM does not receive, on a disaggregated basis, balance sheets, income statements, cash flows (financial statements) and SG&A for the Components. The CODM does not have sufficient information or adequate measures of profitability to assess performance or allocate assets among the Components. Consequently, senior managements’ compensation is determined on the Company’s consolidated results as opposed to the individual component results.

As described above, the CODM uses volume and financial information at the consolidated level for decision making purposes related to the assessment of performance and allocation of resources. The primary focus of the CODM’s review is on volume growth. The CODM does not regularly review information about the Components, and therefore ASC paragraphs 350-20-35-33 through 36 would preclude the Company from identifying the Components as separate reporting units. ASC 350-20-35-36 states that an operating segment shall be deemed to be a reporting unit if all of its components are similar, if none of its components is a reporting unit, or if it comprises only a single component.

Based on the above guidance and discussion, the Company determined that it has a single reporting unit based upon its determination that it has a single operating segment.

• |

Tell us in reasonable detail how you determined the fair value of your reporting unit. Please include the specific method(s) utilized. |

Response

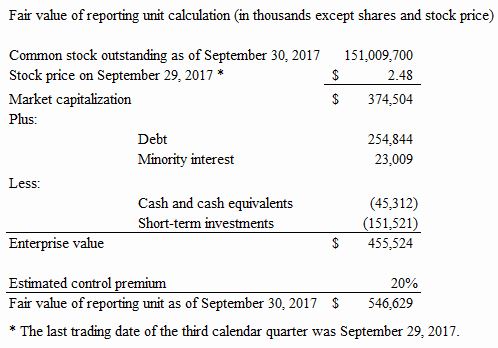

The Company determined the fair value of its reporting unit by calculating the Company’s enterprise value and adding an assumed control premium. The Company utilized this method as enterprise value is commonly used as a valuation metric and the Company’s securities analysts use it in their determinations of stock price targets.

The Company calculated its enterprise value as its market capitalization, plus its total debt and capital lease obligations, plus its minority interest, minus its cash and cash equivalents, and minus its short-term investments as shown in the table below.

4

• |

Tell us the material assumptions used under each method utilized. Examples might include: how cash flows were estimated, the discount rate used, the principal market and market participants selected. Please ensure your response addresses how you determined each of the assumptions used was appropriate. |

Response

As described above, calculating the Company’s enterprise value and adding an assumed control premium was the only method utilized by the Company in determining the fair value of its reporting unit. This calculation involved objective data derived from the Company’s financial statements, as well as an assumed control premium. As a result, such control premium was the only material assumption used in the analysis.

In accordance with ASC 350-20-35-22 and 23 the Company determined that it was appropriate to include a control premium as an acquiring entity often is willing to pay more for equity securities that give it a controlling interest than an investor would pay for a number of equity securities representing less than a controlling interest. That control premium may cause the fair value of a reporting unit to exceed its market capitalization. The quoted market price of an individual equity security, therefore, need not be the sole measurement basis of the fair value of a reporting unit.

To determine an appropriate control premium, the Company analyzed publicly available information about certain completed acquisition transactions. The Company reviewed the control premiums of 15 acquisitions of publicly traded companies in the energy industry, which had a mean and a median premium of 23%.

In addition, the Company also considered its leadership position in the market for natural gas as a vehicle fuel in determining an appropriate control premium. Because the Company is the largest

5

provider of natural gas as an alternative fuel for vehicle fleets in the United States and Canada, based on the number of stations operated and the amount of gasoline gallon equivalents of CNG, LNG and RNG delivered, the Company considered that a larger premium may be needed in order to purchase a controlling stake in the Company. Based on the analysis described above, the Company utilized a control premium of 20% of the Company’s enterprise value as a minimum level of control premium, recognizing that a larger control premium could be justified but such larger control premium would only increase the fair value of the reporting unit.

The Company periodically reviews the assumed control premium used in determining fair value, taking into consideration current industry, market and economic conditions, as well as other factors or available information specific to the Company’s business.

• |

If you utilized multiple approaches in determining fair value, please tell us the relative weighting assigned to each method and how you determined the weighting was appropriate. |

Response

The Company did not use multiple approaches in determining fair value.

• |

Please provide us with a reconciliation of the fair value of your reporting unit to your market capitalization. If applicable, provide support for any control premiums. Refer to ASC 350-20-35-22 and -23. |

Response

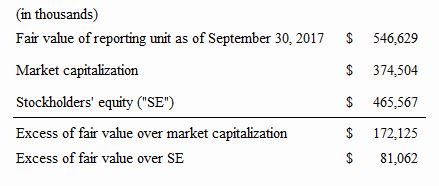

The goodwill impairment test of the Company’s one reporting unit resulted in a fair value of $546.6 million at September 30, 2017 as compared to the Company’s market capitalization of $374.5 million at such date and the Company’s net book value of stockholders’ equity of $465.6 million. The reconciliation of the fair value of the Company’s reporting unit to its market capitalization at September 30, 2017 is as follows:

Please reference the discussion above regarding the Company’s determination that it was appropriate to include a control premium and the support for the control premium used.

6

* * * *

If you have any questions or would like further information concerning the Company’s responses to the Comment Letter, please do not hesitate to contact me at (949) 437-1000.

Sincerely, |

|

|

/s/ Robert M. Vreeland

|

|

|

Robert M. Vreeland

Chief Financial Officer

Clean Energy Fuels Corp.

|

|

cc: Andrew J. Littlefair

J. Nathan Jensen

7